Table of Contents

- Quick Summary

- Why Middle-Class Families in India Are the Most Financially Vulnerable During Medical Emergencies

- The Invisible Gap Nobody Talks About

- Common Costs Included in Medical Emergency Expenses in India

- What Happens When Healthcare Costs Rise Faster Than Salaries?

- Why Insurance Alone May Not Always Be Enough

- How Medical Crowdfunding Helps Manage Medical Emergency Expenses in India

- The Pressure to Appear Fine

- Why Community Support Is Becoming Part of the Response

- Conclusion

- FAQs

Quick Summary

- Medical emergency expenses in India are rising faster than most middle-class families can realistically prepare for.

- Even families with insurance and stable incomes often struggle with uncovered hospital and rehabilitation costs.

- Long-term treatment expenses, EMIs, and existing financial responsibilities leave little room for sudden healthcare crises.

- More families are turning to emergency fundraising and medical crowdfunding platforms to bridge urgent treatment gaps.

- Community-driven support and crowdfunding for health issues are becoming part of how families manage modern medical costs.

Why Middle-Class Families in India Are the Most Financially Vulnerable During Medical Emergencies

A couple of weeks in intensive care is sometimes all it takes to drain a family’s savings.

For many middle-class families in India, this situation feels far more familiar than extreme. A car, regular EMI payments, corporate health insurance, years of careful financial planning, and still, a sudden medical emergency can leave families borrowing lakhs before a loved one is even discharged.

India’s middle class sits in a quietly dangerous financial position. Rising medical emergency expenses in India have made even financially disciplined households vulnerable to sudden healthcare crises. These families are often too financially stable to qualify for assistance, yet not financially protected enough to absorb a medical bill of ₹15–20 lakh without long-term consequences.

This blog explores why medical emergencies affect middle-class families so deeply, from rising healthcare costs and insurance limitations in a country where out-of-pocket healthcare expenses account for 39.4% of total health expenditure, among the highest globally, to the emotional pressure of staying financially afloat during a crisis. It also examines why more families are turning to community-driven support, emergency fundraising, and medical crowdfunding platforms to manage expenses that savings and insurance alone often cannot cover.

The Invisible Gap Nobody Talks About

Most middle-class households look stable from the outside. Salaried income, some savings, maybe a fixed deposit or two. But underneath that, many families run on tightly balanced monthly budgets, home loan EMI, children’s school fees, ageing parents’ maintenance, and household expenses that leave little room for the unexpected.

A medical emergency doesn’t just cost money. It costs money immediately. Advance deposits before admission. Daily consumables not covered by insurance. Attendant fees. Private ambulance charges. Nutrition supplements post-discharge. These costs begin on day one and don’t stop when the patient comes home.

This is where medical emergency expenses in India become especially difficult for middle-class families to absorb. The pressure doesn’t come from a single hospital bill alone, but from the speed, unpredictability, and continuity of healthcare costs during a crisis.

The middle class rarely factors any of this in. And why would they, until it happens?

Common Costs Included in Medical Emergency Expenses in India

Medical emergency expenses in India involve much more than hospital admission fees. Emergency healthcare often includes multiple charges that together create a large financial burden. Some of the most common expenses include:

- Ambulance and emergency transport charges

- Emergency room consultation fees

- ICU and ventilator chargesc

- Doctor and specialist consultation costs

- Surgery and operation theatre fees

- Diagnostic tests such as MRI, CT scans, blood tests, and X-rays

- Medicines and injections

- Hospital room rent and nursing charges

- Post-surgery rehabilitation and physiotherapy

- Follow-up consultations and recovery care

In severe cases, families may also face additional costs related to long-term medication, home nursing, dialysis, chemotherapy, or repeated surgeries. These growing medical emergency expenses in India often leave families financially drained even after the patient recovers.

What Happens When Healthcare Costs Rise Faster Than Salaries?

Medical emergency expenses in India have increased sharply over the last decade, especially in private urban healthcare.

ICU care at a mid-tier private hospital in a metro city now costs ₹15,000 – ₹40,000 per day. A cardiac surgery can run between ₹3–8 lakhs. Cancer treatment, depending on the stage and protocol, can cross ₹20–50 lakhs over a full course. Diagnostics, repeat scans, specialist consultations, and long-term medications, each line item adds up quietly.

Meanwhile, salary growth for many middle-income professionals has remained relatively moderate. Healthcare inflation, however, continues to rise at a much faster pace.

This gap widens every year. And when a medical emergency arrives, families often realise the financial cushion they depended on is far thinner than expected.

Over time, treatment decisions also become financial decisions. Families begin asking difficult questions: can we afford the better implant, should we do the scan now or wait, can we continue treatment for another month?

That mental shift, from what’s medically ideal to what’s financially manageable, is one of the most emotionally exhausting parts of a healthcare crisis.

Why Insurance Alone May Not Always Be Enough

Health insurance remains one of the most important financial protections a family can have. For many households, it significantly reduces the burden of hospitalisation costs. But during serious or long-term illnesses, families often discover that certain expenses still fall outside what policies fully cover.

Room rent limits, co-payment clauses, waiting periods, procedure caps, and exclusions on consumables such as gloves, syringes, or PPE kits can gradually increase out-of-pocket spending during treatment.

Post-hospitalisation care can add further pressure. Physiotherapy, home nursing, rehabilitation, follow-up consultations, and long-term medication expenses are often only partially covered. In conditions like stroke recovery or major orthopaedic procedures, rehabilitation itself may continue for months.

This is why even insured families sometimes find themselves arranging additional funds during medical emergencies. Insurance helps substantially, but rising healthcare costs and extended recovery needs can still create financial gaps that households are unprepared for.

How Medical Crowdfunding Helps Manage Medical Emergency Expenses in India

Medical crowdfunding has become an important financial support system for families facing high treatment costs. Online fundraising platforms allow patients to raise donations from friends, relatives, colleagues, and kind-hearted donors across the country.

Crowdfunding is commonly used for cancer treatment, organ transplants, accident care, neonatal emergencies, rare diseases, and expensive surgeries. Families can share their medical stories online and receive financial help quickly during critical situations.

One of the biggest advantages of crowdfunding is that it reduces the pressure of taking large loans or selling assets. For many families struggling with medical emergency expenses in India, crowdfunding provides immediate financial relief and allows patients to continue life-saving treatment without delays.

The Pressure to Appear Fine

This part is harder to quantify, but just as real.

Middle-class families carry a particular kind of social pressure, the expectation of self-sufficiency. Asking for help, even from close family, feels like an admission of failure. There’s hesitation. Embarrassment. A tendency to exhaust every private option first before saying anything publicly.

Some families quietly liquidate savings. Others break fixed deposits or take informal loans from relatives and colleagues. A few sell assets. Many delay treatment, hoping costs come down, or the situation resolves itself.

By the time they consider broader support, weeks have passed. Debt has accumulated. And the emotional weight of managing a health crisis and a financial crisis simultaneously takes a toll that doesn’t show on any balance sheet.

Why Community Support Is Becoming Part of the Response

When a medical crisis hits, the gap between what insurance covers and what treatment actually costs can open up within days.

Over the last few years, more families have started turning to their networks to bridge exactly that gap. Friends share fundraisers. Colleagues contribute. Strangers respond because the need is documented and the urgency is real.

Medical crowdfunding platforms like ImpactGuru have made emergency fundraising accessible precisely when time matters most. Families can share verified medical documentation and reach hundreds of people within hours, while treatment is still ongoing, not after the crisis has passed.

It sits alongside insurance and savings, not in place of them. But when costs are mounting daily, and every source of support counts, the ability to raise donations online can make a critical difference in whether a family continues treatment without interruption.

It’s not charity in the traditional sense. It’s collective support, the same instinct that drives communities to show up for one another, now operating at a larger scale.

Conclusion

India’s medical emergency financial vulnerability is increasingly running through the middle, through families who did the right things, made responsible choices, and still found themselves unprepared.

Healthcare costs in India have outpaced what most households can realistically absorb. That’s not a personal failure, instead a structural reality that more families are quietly navigating every year.

The cost of waiting to plan, to act, to ask for support, is almost always higher than the cost of starting early. Options exist. The difference is knowing them at the right time.

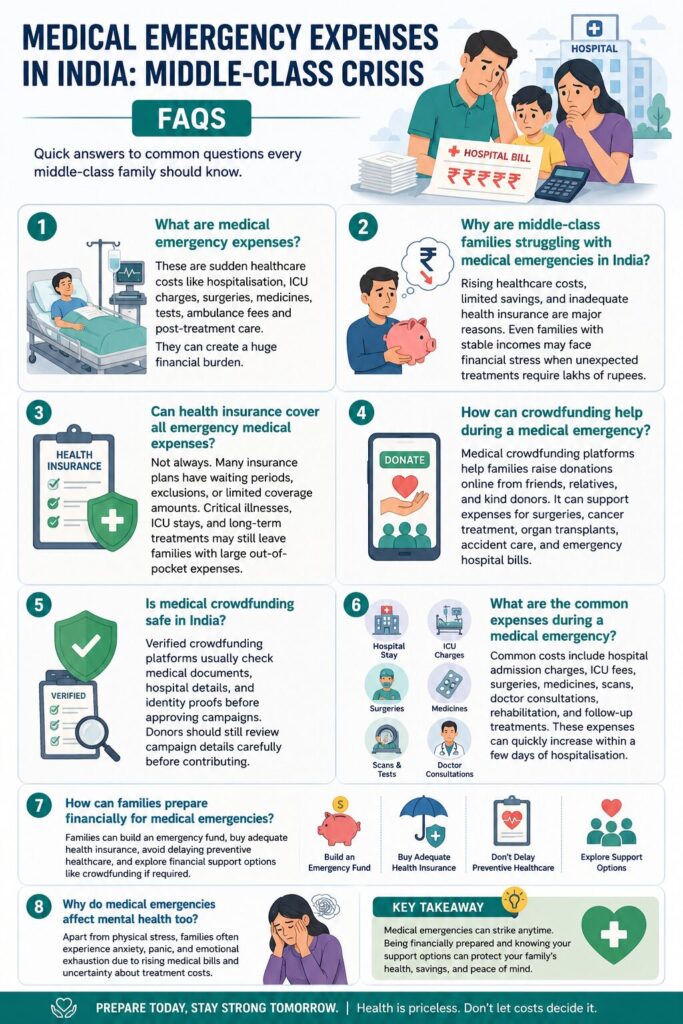

FAQs

Medical emergency expenses include sudden healthcare costs such as hospitalisation, ICU charges, surgeries, medicines, diagnostic tests, ambulance fees, and post-treatment care. These expenses can create a huge financial burden for middle-class families in India.

Rising healthcare costs, limited savings, and inadequate health insurance are major reasons. Even families with stable incomes may face financial stress when unexpected treatments require lakhs of rupees.

Not always. Many insurance plans have waiting periods, exclusions, or limited coverage amounts. Critical illnesses, ICU stays, and long-term treatments may still leave families with large out-of-pocket expenses.

Medical crowdfunding platforms help families raise donations online from friends, relatives, and kind donors. It can support expenses for surgeries, cancer treatment, organ transplants, accident care, and emergency hospital bills.

Verified crowdfunding platforms usually check medical documents, hospital details, and identity proofs before approving campaigns. Donors should still review campaign details carefully before contributing.

Common costs include hospital admission charges, ICU fees, surgeries, medicines, scans, doctor consultations, rehabilitation, and follow-up treatments. These expenses can quickly increase within a few days of hospitalisation.