Table of Contents

- Quick Summary

- Introduction

- What Is the Fibroid Surgery Cost in India? A Full Breakdown

- Does Insurance Cover Fibroid Surgery in India?

- How to Reduce Fibroid Surgery Expenses in India

- What Are the Financing Options for Fibroid Surgery in India?

- How to Pay for Fibroid Removal Surgery Without Insurance

- How to Afford Fibroid Surgery in India: Insurance, EMI & Crowdfunding

- Conclusion

- FAQs

Quick Summary

- Fibroid surgery cost in India ranges from ₹50,000 to ₹1,15,000+, depending on the procedure type, city, and hospital tier.

- Health insurance may cover fibroid surgery if medically certified. Understanding your policy can save you lakhs.

- Government schemes like Ayushman Bharat and state-level programmes offer significant financial relief.

- Medical loans, hospital EMI plans, and health credit cards are practical financing alternatives.

- Crowdfunding on Indian platforms has helped thousands of patients raise funds for major surgeries quickly.

Introduction

A fibroid diagnosis can feel overwhelming, not just physically, but emotionally, too. From heavy bleeding and chronic pain to fatigue and discomfort, uterine fibroids can quietly disrupt your daily life and overall well-being. When your gynaecologist recommends surgery, it’s often not just a medical suggestion; it’s a step toward getting your health, energy, and peace of mind back.

But alongside the decision to prioritise your health comes a very real concern: the fibroid surgery cost in India. For many women, this becomes an added layer of stress during an already difficult time.

You’re not alone. Thousands of women across India face this exact situation every year, balancing the need for timely treatment with the worry of affordability. The reality is that the uterine fibroid surgery cost in India can vary widely depending on the type of procedure, hospital, and city. Without clear guidance, it’s easy to feel confused, delay treatment, or settle for less-than-ideal options.

This guide is here to support you through both your health decision and your financial planning. From understanding surgery costs to exploring insurance, financing, and fundraising options, we’ll walk you through everything you need to make informed, confident choices.

Because taking care of your health shouldn’t feel out of reach.

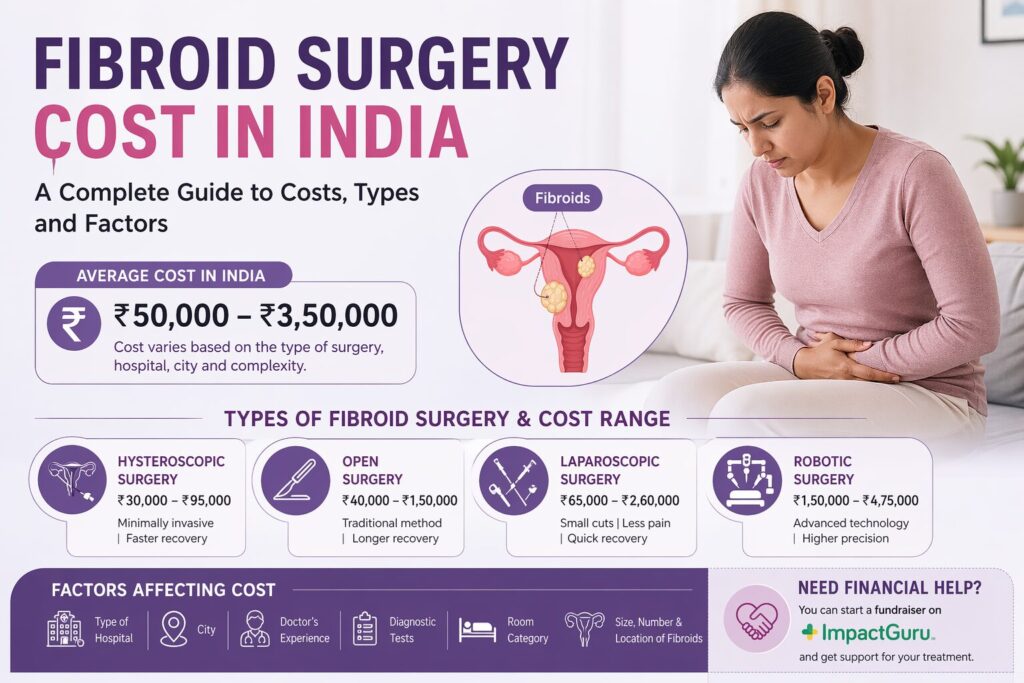

What Is the Fibroid Surgery Cost in India? A Full Breakdown

Quick Answer: Fibroid surgery cost in India typically ranges from ₹50,000 to ₹1,15,000+, depending on procedure type, hospital tier, and city. Laparoscopic surgery costs more upfront but offers faster recovery. Government hospitals are significantly more affordable than private ones.

Click here to find hospitals near you!

Understanding uterine fibroid surgery cost in India starts with recognising that there is no single number. The cost of fibroid removal surgery is shaped by several variables: the type of procedure your doctor recommends, the kind of hospital you choose, the city you’re in, and how complex your case is.

Here’s a clear breakdown to give you a realistic starting point:

Surgery Type vs. Estimated Cost

| Surgery Type | Estimated Cost |

| Open Myomectomy | ₹93,000 – ₹1,10,000 |

| Laparoscopic Myomectomy | ₹45,000 – ₹1,30,000 |

| Hysteroscopic Myomectomy | ₹50,000 – ₹1,50,000 |

Note: These are indicative ranges. Always get a written cost estimate from your hospital before proceeding.

What Drives the Cost Up?

Several factors push the final bill higher than the base procedure cost:

- Surgeon’s experience and reputation – A senior gynaecological surgeon at a reputed private hospital will charge significantly more than a consultant at a district hospital. The premium is often justified by skill and outcomes, but not always necessary for straightforward cases.

- City and hospital tier – Laparoscopic fibroid surgery cost in metros like Mumbai, Delhi, and Bengaluru runs 30–50% higher than the same procedure in Tier-2 cities like Nagpur, Coimbatore, or Jaipur. If travel and accommodation are manageable, a planned surgery in a Tier-2 city can result in meaningful savings.

- Anaesthesia and OT charges – These are often listed separately and can add ₹15,000 to ₹40,000 to your bill, depending on the duration of surgery.

- Duration of hospital stay – Open surgeries typically require 3–5 days of hospitalisation. Laparoscopic procedures may require only 1–2 days. Each additional day adds room charges, nursing fees, and medication costs.

- Pre-operative diagnostics – Ultrasounds, MRIs, blood panels, and ECGs are required before surgery and may or may not be included in the hospital’s quoted package. Always ask specifically what the quote includes.

- Post-operative care and medication – Discharge prescriptions, follow-up consultations, and any complications can add to the overall cost of fibroid removal surgery.

City-Wise Cost Snapshot

| City | Approximate Range (Private Hospital) |

| Mumbai | ₹55,000 – ₹3,50,000 |

| Delhi / NCR | ₹68,000 – ₹3,00,000 |

| Bengaluru | ₹70,000 – ₹3,50,000 |

| Chennai | ₹60,000 – ₹3,50,000 |

| Hyderabad | ₹58,000 – ₹3,50,000 |

| Pune | ₹52,000 – ₹3,50,000 |

| Tier-2 Cities | ₹55,000 – ₹3,50,000 |

The hysterectomy cost in India follows a similar city-wise pattern, with total costs in metro private hospitals reaching ₹3,00,000 or more when you factor in extended hospital stay and post-operative care.

One Important Note

Always ask for an itemised cost estimate in writing before signing any consent or paying any advance. Many hospitals offer “package rates” that bundle the major costs together — these can be good value, but only if you verify what is and isn’t included. Hidden charges around consumables, ICU use, or specialist consultations can surface at billing time and catch patients off guard.

Does Insurance Cover Fibroid Surgery in India?

Quick Answer: Yes, most health insurance policies in India cover fibroid surgery if it is medically necessary. You’ll need a gynaecologist’s certificate confirming the diagnosis, and in most cases, pre-authorisation from your insurer before the surgery date. Cosmetic or elective procedures may not qualify.

For many women, health insurance is the single biggest lever for reducing out-of-pocket fibroid surgery costs. Yet a large number of patients either don’t know their policy covers it, or lose their claim due to avoidable paperwork errors. Understanding how insurance coverage for fibroid surgery works in India can save you anywhere from ₹50,000 to ₹2,00,000.

What “Medically Necessary” Actually Means

Insurance companies in India don’t cover every surgery automatically. They cover medically necessary procedures — meaning your doctor has determined that surgery is required to treat a condition that is causing a significant health impact. For fibroids, this typically means:

- Heavy menstrual bleeding that affects daily functioning

- Pelvic pain or pressure that hasn’t responded to medication

- Fibroids causing fertility issues or pregnancy complications

- Rapid fibroid growth or suspicion of malignancy

If your gynaecologist has documented any of these in your case file, your surgery is almost certainly classifiable as medically necessary, which is the foundation of a successful insurance claim.

Which Policies Cover Fibroid Surgery?

| Policy Type | Coverage Likelihood |

| Individual Health Insurance | Covered after waiting period (usually 2–4 years) |

| Family Floater Policy | Covered under the same waiting period terms |

| Corporate / Group Health Insurance | Often covers pre-existing conditions from Day 1 |

| Government Employee Schemes (CGHS/ECHS) | Covered at empanelled hospitals |

| Ayushman Bharat – PM-JAY | Covered for eligible BPL families |

The most important thing to check is your policy’s pre-existing disease (PED) waiting period. If fibroids were diagnosed before you took out your policy, most insurers apply a waiting period of 2 to 4 years before they’ll cover related treatment. If you’re past that window, you’re in a strong position to claim.

Read More : Crowdfunding for Cancer in India: Reality Check, Success Rates, Challenges & Costs (2026)

What Is Typically Covered

Most standard health insurance policies in India will cover the following components of fibroid surgery:

- Surgeon’s fees and assistant surgeon charges

- Anaesthesia charges

- Operation theatre fees

- In-patient hospitalisation (room rent, nursing, meals)

- Pre-hospitalisation expenses up to 30 days before admission

- Post-hospitalisation expenses up to 60 days after discharge

- Blood transfusions and consumables used during surgery

What Is Typically Not Covered

- OPD consultations and routine check-ups before admission

- Diagnostic tests done on an outpatient basis (unless your policy has an OPD rider)

- Non-medical expenses: attendant charges, telephone, toiletries

- Treatment during the waiting period for pre-existing conditions

- Procedures classified as cosmetic or not medically justified

How to Reduce Fibroid Surgery Expenses in India

You can reduce fibroid surgery expenses in India by choosing government or charitable trust hospitals, comparing quotes across multiple facilities, using your insurance fully, and timing your surgery after your policy’s waiting period. Asking for itemised billing and avoiding unnecessary add-ons can also cut costs significantly.

Even with insurance, most patients end up paying something out-of-pocket. And for those without coverage, every rupee saved matters. Here are practical, proven ways to bring down your total cost.

Choose the Right Hospital for Your Case

Not every fibroid case requires a premium private hospital. Government medical colleges and charitable trust hospitals, such as those run by religious trusts or municipal corporations, offer the same surgical procedures at a fraction of the cost. The infrastructure may be more basic, but for a straightforward myomectomy or hysterectomy, the clinical outcome is often comparable.

Some well-regarded options include government medical college hospitals in every state, as well as trust-run hospitals like Tata Memorial-affiliated centres, Wockhardt Foundation clinics, and municipal corporation hospitals in metro cities.

Get Multiple Quotes — and Ask the Right Questions

Call or visit at least 2–3 hospitals before deciding. When you ask for a quote, specifically request:

- An all-inclusive package cost

- What is and isn’t included in the package

- Whether the surgeon quoted is the one who will actually perform the surgery

- What the policy is if complications arise and additional procedures are needed

This comparison exercise alone can reveal price differences of ₹40,000 to ₹80,000 for the same procedure in the same city.

Ask for Itemised Billing

Package rates are convenient but can obscure inflated line items. Ask for an itemised bill and review it carefully. Duplicate charges, unnecessary consumables, and inflated medication costs are not uncommon. You have every right to question and dispute charges that seem incorrect or excessive.

Consider Medical Travel Within India

If you live in a metro city, the same surgery performed at a reputed hospital in a Tier-2 city could cost 30–50% less. Factor in travel and accommodation, and you may still come out significantly ahead. Cities like Coimbatore, Nashik, Vadodara, and Kochi have excellent private hospitals with experienced gynaecological surgeons at much lower price points than Mumbai or Delhi.

Use Your Employer’s Group Insurance Fully

Many salaried employees have group health insurance through their employer that covers pre-existing conditions from Day 1 — unlike individual policies. If you’re employed, check with your HR department about the exact coverage, sum insured, and network hospitals before making any decision about where to get treated.

What Are the Financing Options for Fibroid Surgery in India?

Financing options for fibroid surgery in India include hospital EMI schemes, medical loans from banks and NBFCs, health credit cards, and government schemes like Ayushman Bharat. Many private hospitals now offer no-cost EMI for planned surgeries, making it possible to spread costs over 6 to 24 months without a heavy interest burden.

Not everyone has a lump sum ready when surgery is needed. The good news is that the medical financing landscape in India has expanded significantly over the last decade. You don’t have to drain your savings or borrow from family — there are structured, dignified options available that let you get treated now and pay over time.

Here’s a comprehensive look at every financing option worth considering.

1. Hospital EMI and No-Cost EMI Plans

Many private hospitals — especially larger chains like Apollo, Fortis, Manipal, and Max — have tie-ups with banks and NBFCs to offer EMI payment plans directly at the billing counter. These can be:

- No-cost EMI — where the interest is absorbed by the hospital or the financing partner, and you pay only the principal split across months (typically 3, 6, or 9 months)

- Low-interest EMI — for longer tenures of 12 to 24 months, a nominal interest rate applies

To access this, you typically need a credit card from a partnering bank (HDFC, ICICI, SBI, Axis are common). Ask the hospital’s billing department specifically about EMI options before your admission date — not after, when you’re already under pressure.

What to ask the hospital:

- Which banks and cards are eligible for no-cost EMI?

- What is the minimum transaction amount for EMI conversion?

- Are there any processing fees?

2. Medical Loans from Banks and NBFCs

If you don’t have a credit card or need a larger amount, a personal loan or dedicated medical loan is a strong option. Several banks and Non-Banking Financial Companies (NBFCs) offer these with relatively quick disbursal.

Tips for getting a medical loan quickly:

- Keep your Aadhaar, PAN, last 3 months’ salary slips, and bank statements ready

- A credit score above 700 significantly improves your approval chances and interest rate

3. Health Credit Cards and Medical Finance Cards

A growing category of financial products specifically designed for healthcare expenses. The most widely used in India include:

Bajaj Finserv Health EMI Card — Offers a pre-approved credit limit for medical expenses at partner hospitals. Can be used for surgery, diagnostics, and post-operative care. EMI tenures range from 3 to 24 months.

Pine Labs / Svaas Health Finance — Available at several hospital chains, allowing patients to convert large medical bills into manageable monthly payments at the point of care.

These cards are worth getting even before a health emergency arises, as the application and approval process takes time.

4. Government Schemes That Can Cover Fibroid Surgery

This is the most underutilised category of financial help in India — largely because awareness is low. If you or your family qualify, government schemes can cover the entire cost of fibroid surgery.

Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana (PM-JAY)

India’s flagship health insurance scheme covers hospitalisation costs up to ₹5 lakh per family per year for eligible beneficiaries. Fibroid surgeries — including hysterectomy and myomectomy — are included in the procedure list.

Who is eligible:

- Families listed in the Socio-Economic Caste Census (SECC) 2011 database

- BPL (Below Poverty Line) cardholders

- Families in specified occupational categories (construction workers, ragpickers, domestic helpers, etc.)

State-Level Health Schemes

How to check eligibility and use it:

- Visit pmjay.gov.in and check using your mobile number or ration card

- If eligible, get your Ayushman card made at a Common Service Centre (CSC) or an empanelled hospital

- Choose a PM-JAY empanelled hospital for your surgery — the entire cost is cashless and covered

Several states have their own schemes that either supplement PM-JAY or operate independently:

| State | Scheme Name | Coverage |

| Maharashtra | Mahatma Jyotiba Phule Jan Arogya Yojana | Up to ₹1.5 lakh per year |

| Tamil Nadu | Chief Minister’s Comprehensive Health Insurance | Up to ₹5 lakh per family |

| Andhra Pradesh | YSR Aarogyasri | Covers 2,500+ procedures |

| Karnataka | Arogya Karnataka | Universal coverage for residents |

| Delhi | Delhi Arogya Kosh | Financial aid for serious illnesses |

If you’re unsure which scheme applies to you, visit your nearest government hospital’s help desk; they are required to guide patients on eligibility.

Chief Minister’s / PM’s Relief Fund

Both state and central relief funds accept applications from patients who cannot afford treatment. These are discretionary but frequently granted for medically urgent cases. Your application should include:

- A letter from your gynaecologist stating medical urgency

- An income certificate or BPL card

- A cost estimate from the hospital

- A personal letter explaining your financial situation

Applications can be submitted through your local MLA’s or MP’s office, which often speeds up processing.

How to Pay for Fibroid Removal Surgery Without Insurance

Quick Answer: Without insurance, your best options are government hospital subsidised treatment, Ayushman Bharat for eligible families, medical loans, NGO-backed patient assistance programmes, and medical crowdfunding. BPL cardholders can often access fibroid surgery at government hospitals at little to no cost.

Not having health insurance doesn’t mean surgery is out of reach. It does mean you need to be more proactive about finding the right resources. Here’s how to navigate fibroid surgery costs without an insurance safety net.

Government Hospitals — Your Most Powerful Resource

Every district in India has at least one government hospital where surgery is available at heavily subsidised or zero cost for patients who qualify. At All India Institute of Medical Sciences (AIIMS), Government Medical College hospitals, and district hospitals:

- BPL cardholders often pay nothing beyond a nominal registration fee

- Medicines are dispensed free or at MRP from hospital pharmacies

- Surgery waiting lists exist, but can be navigated with proper documentation

The clinical quality at top government medical colleges, AIIMS Delhi, JIPMER Puducherry, Grant Medical College Mumbai, and Madras Medical College, is genuinely world-class. The experience may differ from a private hospital, but the surgical outcomes frequently don’t.

NGOs and Patient Assistance Programmes

Several NGOs and charitable organisations specifically support women’s health interventions in India:

- SEWA (Self-Employed Women’s Association) — Provides health support and referrals for low-income women

- iCall and similar organisations — Can help navigate the healthcare system and connect patients to subsidised care

- Hospital-run charitable trusts — Many large private hospitals (Tata, Kokilaben, CMC Vellore) have trust funds that subsidise treatment for patients who can demonstrate financial need. Ask to speak with the hospital’s social worker or medical social services department.

How to Apply for Financial Assistance at Private Hospitals

This is a lesser-known but very real option. Most large private hospitals in India have a medical social worker on staff whose job is to help patients access financial support — including internal hospital charity funds, government scheme linkages, and NGO referrals. To access this:

- Ask at the hospital’s front desk or patient services desk to speak with a medical social worker

- Bring all income and financial documents

- Be honest and clear about your situation. These professionals are trained to help, not judge

How to Afford Fibroid Surgery in India: Insurance, EMI & Crowdfunding

The best way to manage the fibroid surgery cost in India is to combine insurance, EMI options, and medical crowdfunding instead of relying on a single source.

If your insurance doesn’t cover the full amount, you can split the cost across multiple options.

Example (₹2,00,000 Surgery)

| Source | Amount Covered |

| Health Insurance | ₹80,000–₹90,000 |

| EMI / Medical Loan | ₹50,000–₹60,000 |

| Medical Crowdfunding | ₹40,000–₹60,000 |

| Total | ₹2,00,000 |

Where Crowdfunding Helps

Medical crowdfunding in India allows you to raise funds by sharing your story on crowdfunding platforms in India.

You typically need:

- Doctor’s diagnosis

- Cost estimate

- A clear explanation of the need

Funds are transferred directly to your bank account, often within days, with no upfront fees on most fundraising platforms in India.

You don’t need one perfect solution, just the right combination.

Conclusion

Fibroid surgery is not a luxury. It is medically necessary care that improves quality of life, preserves fertility, and in some cases prevents serious complications. The cost of that care should not be a reason to delay or avoid it.

The fibroid surgery cost in India, whether it’s ₹70,000 at a government hospital or ₹2,50,000 at a private one, is a number that can be managed with the right combination of information and action. Health insurance, government schemes, medical loans, hospital EMI plans, and medical crowdfunding are not fallback options for people who “couldn’t afford it.” They are legitimate, widely used financial tools that exist precisely for situations like this.

You now have a complete picture of what fibroid surgery costs, what insurance covers, what the government provides, and how your community can step in when needed. The next step is yours.

If surgery has been recommended and cost is the only thing standing in the way, start today. Check your insurance policy. Look up your PM-JAY eligibility. Talk to your hospital’s billing desk about EMI. And if you need to raise funds, start your medical crowdfunding campaign now, while there’s still time to build momentum before your admission date.

You deserve the care. The resources exist. Use them.

FAQs

Fibroid surgery in India typically costs between ₹50,000 and ₹3,50,000, depending on the type of surgery, hospital, and city.

The best surgery depends on your condition. Laparoscopic and hysteroscopic surgeries are preferred for faster recovery, while open surgery is used for complex cases.

Yes, most health insurance plans in India cover fibroid surgery if it is medically necessary and not for cosmetic reasons.

Recovery time varies by procedure—hysteroscopic surgery may take a few days, while open surgery can take 4–6 weeks.

You can explore options like medical crowdfunding, insurance, or financial assistance programs to manage fibroid surgery costs.