Table of Contents

- Quick Summary

- Introduction

- What Is OPD and IPD?

- OPD vs IPD – Key Differences

- What Happens in an OPD Consultation? (Step-by-Step)

- When Is IPD Admission Required? Understanding Inpatient Care

- OPD and IPD Charges Difference – What You’re Actually Paying For

- Does Health Insurance Cover OPD and IPD in India?

- How Do Hospitals Classify OPD and IPD Patients?

- Why OPD vs IPD Matters for Medical Bills

- How Medical Crowdfunding Fills the Gap

- Outpatient and Inpatient Difference – Quick Reference for Common Conditions

- Conclusion

- FAQs

Quick Summary

- The difference between OPD vs IPD comes down to one thing: whether you stay overnight in a hospital or walk out the same day.

- OPD stands for Outpatient Department, consultations, diagnostics, and minor procedures that don’t need admission

- IPD stands for Inpatient Department, where patients are formally admitted, assigned a bed, and monitored continuously

- OPD visits are generally cheaper; IPD stays involve room charges, nursing care, surgery costs, and more

- Health insurance policies in India often cover IPD fully, but may have limited or add-on OPD coverage. Knowing the difference can save you money.

Introduction

You’ve seen both terms on hospital boards, insurance documents, and medical bills, OPD and IPD. Most people nod along without really knowing what separates the two. And honestly? That gap in understanding can cost you.

In this blog, we will understand what OPD and IPD mean, how Indian hospitals classify patients into these categories, what the charges typically look like, and how insurance treats both categories differently. We’ve also addressed what happens when a medical emergency turns into a prolonged hospital stay, and how families manage unexpected costs when coverage falls short. By the end, you’ll know exactly which department applies to your situation and what to expect financially.

What Is OPD and IPD?

OPD (Outpatient Department) is where patients visit for consultations, tests, or minor treatments without being admitted. IPD (Inpatient Department) involves formal hospital admission with a bed, continuous monitoring, and usually an overnight or multi-day stay.

OPD Full Form in Hospital: Outpatient Department

In an OPD setting, you arrive at the hospital, see a doctor, get your prescription or test done, and leave. The entire interaction is self-contained. No bed is assigned to you. You’re not part of the hospital’s ward system.

IPD Full Form in Hospital: Inpatient Department

IPD works differently. Once you’re admitted, whether it’s for surgery, a serious illness, or a condition that needs close observation, you become an inpatient. A bed is allocated, a case file is opened, and a care team monitors you around the clock until you’re discharged.

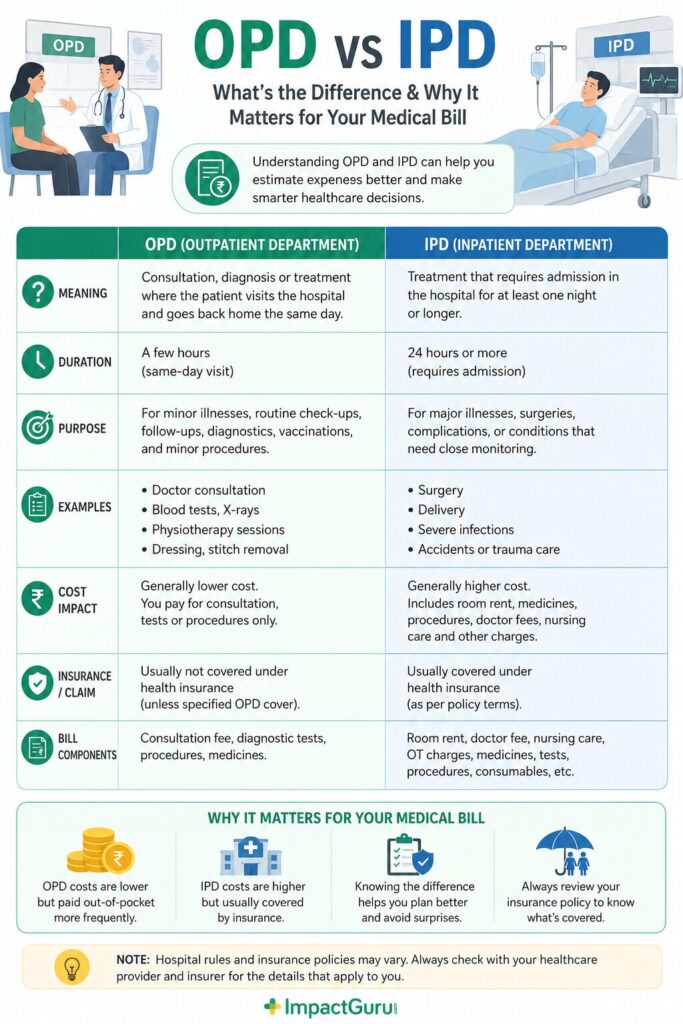

OPD vs IPD – Key Differences

OPD and IPD differ in admission status, charges, insurance coverage, and care intensity. OPD is for same-day, non-critical visits. IPD involves admission, a higher cost structure, and more comprehensive insurance benefits under most Indian health policies.

Here’s a structured comparison that makes the distinction crystal clear:

| Parameter | OPD | IPD |

| Admission required? | No | Yes |

| Bed assigned? | No | Yes |

| Duration | Few hours | 1 day to several weeks |

| Monitoring | Self-managed | Continuous clinical monitoring |

| Typical use | Consultations, tests, vaccinations | Surgery, serious illness, childbirth |

| Billing structure | Per service/consultation | Room rent + nursing + procedure fees |

| Insurance coverage in India | Limited / add-on | Usually covered from day 1 or day 2 |

| Discharge process | Walk out after the visit | The formal discharge summary is required |

The billing difference alone is significant. An OPD consultation might cost ₹300–₹1,500 at a private hospital. An IPD stay for even a straightforward procedure, say, appendix removal, can run anywhere from ₹40,000 to ₹2,00,000+, depending on the hospital tier and city.

What Happens in an OPD Consultation? (Step-by-Step)

An OPD consultation typically involves registration, a doctor visit, diagnosis or test referral, and a prescription, all completed in one visit. No admission paperwork is involved, and you leave the hospital the same day.

Here’s how a standard OPD visit unfolds in most Indian hospitals:

Step 1 – Registration: You register at the OPD counter (or online, in many hospitals now) and receive a token or appointment number. A nominal OPD registration fee is charged, usually ₹100–₹500 in private facilities.

Step 2 – Doctor Consultation: You meet the specialist or general physician. They review your symptoms, history, and any prior reports. The consultation lasts 10–30 minutes, depending on complexity.

Step 3 – Tests or Referrals (if needed): If blood work, imaging, or a specialist referral is required, you go to the respective departments within the hospital, still as an outpatient.

Step 4 – Prescription / Treatment Plan: You leave with a prescription, a follow-up date, or a referral letter. If a minor procedure is done (wound dressing, injection, IV drip), it’s still classified as OPD as long as you aren’t admitted.

Step 5 – Billing and Exit: You pay at the OPD billing counter for the consultation and any services used, then walk out.

No admission. No ward. No overnight stay. That’s the essence of OPD.

When Is IPD Admission Required? Understanding Inpatient Care

IPD admission is required when a patient’s condition needs continuous monitoring, surgical intervention, or treatments that can’t safely be completed in a single visit. Emergencies, planned surgeries, childbirth, and serious infections typically require inpatient admission.

Not every hospital visit needs admission, but some conditions simply can’t be managed from home or through periodic checkups. Here’s when IPD becomes necessary:

- Planned Surgeries: Any procedure requiring general or spinal anaesthesia, knee replacement, hernia repair, or caesarean section will automatically trigger IPD admission. Pre-operative tests are usually done via OPD; the actual procedure shifts you into IPD.

- Medical Emergencies: Heart attacks, strokes, severe infections, fractures, these require immediate admission, stabilisation, and multi-day care. You may enter through the Emergency Department, but be formally converted to IPD once your condition is assessed.

- Chronic Disease Management: Conditions like uncontrolled diabetes, kidney failure requiring dialysis setup, or cancer treatment cycles often require periodic IPD admissions even if you’re managing day-to-day as an outpatient.

- Childbirth: Whether normal delivery or C-section, childbirth is always classified under IPD. The mother is formally admitted, and the baby gets a separate IPD record too.

- Observation / Monitoring: Sometimes doctors aren’t sure if a condition will stabilise or worsen. In such cases, a 24–48 hour observation admission is recommended, still classified as IPD.

- A good rule of thumb: if the doctor says “we’ll need to keep you,” you’re moving from OPD territory into IPD.

OPD and IPD Charges Difference – What You’re Actually Paying For

OPD charges cover consultation fees and specific services used per visit. IPD charges are multi-layered, including room rent, nursing charges, surgery fees, anaesthesia, medicines, and post-operative care. IPD billing is significantly higher and more complex.

Medical billing in India can feel opaque. Here’s a realistic breakdown:

Typical OPD Charges Include:

- Registration/consultation fee

- Diagnostic test fees (blood, urine, X-ray, ECG)

- Minor procedure charges

- Medicines dispensed at the hospital pharmacy

Typical IPD Charges Include:

- Room rent (general ward, semi-private, private, ICU)

- Nursing and attendant charges

- Surgeon’s / specialist’s fee

- Anaesthesia fee (if applicable)

- OT (operating theatre) charges

- Medicines and consumables

- Diagnostic tests conducted during the stay

- Discharge summary and documentation fees

The cost difference can be dramatic. A routine OPD diabetes consultation might cost ₹800 total. Managing a diabetic foot infection as an inpatient could run ₹1.5 lakh or more over a 10-day stay.

This is where financial planning and medical coverage become non-negotiable.

Does Health Insurance Cover OPD and IPD in India?

Most Indian health insurance plans fully cover IPD expenses after a minimum 24-hour hospitalisation. OPD coverage is less common and usually available as an add-on rider. Always read your policy document carefully before assuming coverage.

This is one of the most searched questions, and the answer depends on your specific policy. Here’s the general picture:

- IPD Coverage: The majority of individual and family floater health insurance plans in India cover inpatient hospitalisation. The standard threshold is 24 hours of continuous admission (day-care procedures are sometimes covered separately). What’s typically covered: room rent (subject to limits), surgeon fees, ICU charges, medicines, and pre/post-hospitalisation expenses.

- OPD Coverage: Standard plans often exclude OPD entirely. You pay consultation fees and diagnostic costs out of pocket. Some insurers, Niva Bupa, Star Health, HDFC ERGO, offer OPD riders or comprehensive plans that include outpatient benefits, but premiums are higher.

What’s Often Missed:

- Pre-hospitalisation OPD expenses (say, tests done 30 days before surgery) are covered by many policies

- Post-hospitalisation OPD follow-ups (usually 60–90 days after discharge) are also covered under most IPD-linked policies

- Cashless vs reimbursement: IPD at network hospitals usually means cashless; OPD reimbursement involves submitting bills manually

Important: Always verify your Sum Insured sub-limits, room rent caps, and disease-specific waiting periods before a planned admission.

How Do Hospitals Classify OPD and IPD Patients?

Hospitals classify patients as OPD or IPD based on whether the treating doctor issues a formal admission order. The admission order triggers bed allocation, a unique IPD number, and a different billing structure.

The OPD vs IPD classification has operational and financial consequences within a hospital.

The Classification Process:

When you arrive at a hospital, you’re registered as an OPD patient by default. A doctor evaluates you. If the doctor determines that your condition requires admission, they issue an admission order. This is the formal trigger that converts your status to IPD.

An IPD number is generated. A ward or room is assigned. Your case moves under the purview of the nursing station, ward doctors, and the hospital’s inpatient management system.

This classification matters because:

- Your insurance company will only process IPD claims if the admission order exists

- The Discharge Summary (a document summarising your entire IPD episode) is mandatory for insurance reimbursement

- Government hospitals also distinguish OPD and IPD for allocation of beds, medicines from the hospital pharmacy, and reporting to health authorities.

In AYUSHMAN BHARAT (PM-JAY) and state government schemes, IPD admissions are tracked separately and have specific empanelment criteria. OPD services under government schemes are handled through Health and Wellness Centres (HWCs) or PHCs, not the main hospital IPD system.

Why OPD vs IPD Matters for Medical Bills

Understanding OPD vs IPD can help patients estimate healthcare expenses more accurately. Since IPD treatments involve hospitalization, the costs are usually much higher than OPD treatments. Additionally, insurance companies process claims differently for OPD and IPD services. Patients who misunderstand these categories may face rejected claims or unexpected out-of-pocket expenses.

For example, a routine doctor consultation for fever usually falls under OPD, while appendicitis surgery requiring hospitalization is categorized as IPD. This classification directly impacts insurance reimbursement and the total treatment cost.

How Medical Crowdfunding Fills the Gap

Even with health insurance, large IPD bills can leave families scrambling. Sub-limits on room rent, disease-specific waiting periods, policy exclusions, and co-payment clauses mean the out-of-pocket component can still be significant.

This is a reality millions of Indian families face every year, not because they were careless, but because medical costs have simply outpaced coverage.

Medical crowdfunding has emerged as a genuine financial lifeline in these situations. Platforms like ImpactGuru allow patients and their families to create fundraisers for critical treatments, cancer surgeries, organ transplants, rare disease management, neonatal ICU care, and receive contributions from people across India and the world.

Unlike loans, funds raised through crowdfunding for health issues don’t need to be repaid. Unlike charity, they’re driven by personal stories that connect donors directly to the patient. And unlike waiting for government schemes (which can take time), a well-run fundraiser can raise significant amounts within days.

For IPD-heavy conditions, where costs pile up fast, and families have little time to arrange funds, crowdfunding for medical treatment has become a parallel safety net. It doesn’t replace insurance, but it bridges the gap that insurance leaves behind.

If you’re supporting a family member through a prolonged hospital stay, it’s worth knowing that ImpactGuru medical crowdfunding platforms exist, are free to start, and can be set up in under 10 minutes.

Outpatient and Inpatient Difference – Quick Reference for Common Conditions

Not sure which category your situation falls under? Here’s a quick reference:

| Condition / Situation | OPD or IPD? |

| Fever consultation | OPD |

| Dengue with low platelets | IPD |

| Routine diabetes checkup | OPD |

| Uncontrolled diabetes needing IV medication | IPD |

| Cataract surgery (day care) | Day Care / IPD |

| Fracture requiring surgery | IPD |

| Prenatal checkup | OPD |

| Delivery (normal or C-section) | IPD |

| Vaccination | OPD |

| Cancer chemotherapy cycle | IPD (Day Care in some cases) |

| Physiotherapy session | OPD |

| Post-surgery follow-up visit | OPD |

The grey zone is day-care procedures, treatments completed in under 24 hours but still requiring formal admission (like cataract surgery or certain cancer infusions). Most insurance policies have a specific daycare list. Check yours.

Conclusion

The difference between OPD and IPD shapes your care experience, your hospital bill, and what your insurance will reimburse. OPD keeps things quick and outpatient. IPD means admission, deeper care, and significantly higher costs.

Understanding this distinction helps you ask the right questions before a planned procedure, read your insurance policy more accurately, and avoid billing surprises.

But insurance has limits. When an IPD stay runs longer than expected, or a critical diagnosis demands treatment that coverage doesn’t fully fund, families need options. Medical crowdfunding has helped thousands of Indian families bridge that exact gap, not as a last resort, but as a practical, dignified tool. Knowing your options, medical and financial, is half the battle.

FAQs

OPD (Outpatient Department) involves treatment without hospital admission, while IPD (Inpatient Department) requires admission and hospital stay.

OPD refers to consultations, diagnostic tests, minor procedures, and treatments where the patient goes home the same day.

IPD treatment includes hospitalization for serious illnesses, surgeries, ICU care, or treatments needing continuous monitoring.

Some health insurance plans cover OPD expenses, but many policies offer it as an add-on benefit.

In most cases, IPD involves hospitalization for 24 hours or more, though some daycare procedures may also qualify.

Doctor consultations, blood tests, X-rays, physiotherapy, and minor treatments are common OPD services.