Table of Contents

- Quick Summary

- How Can Families Manage Expensive Treatment Costs Without Insurance

- Why Medical Bills Hit So Hard in India

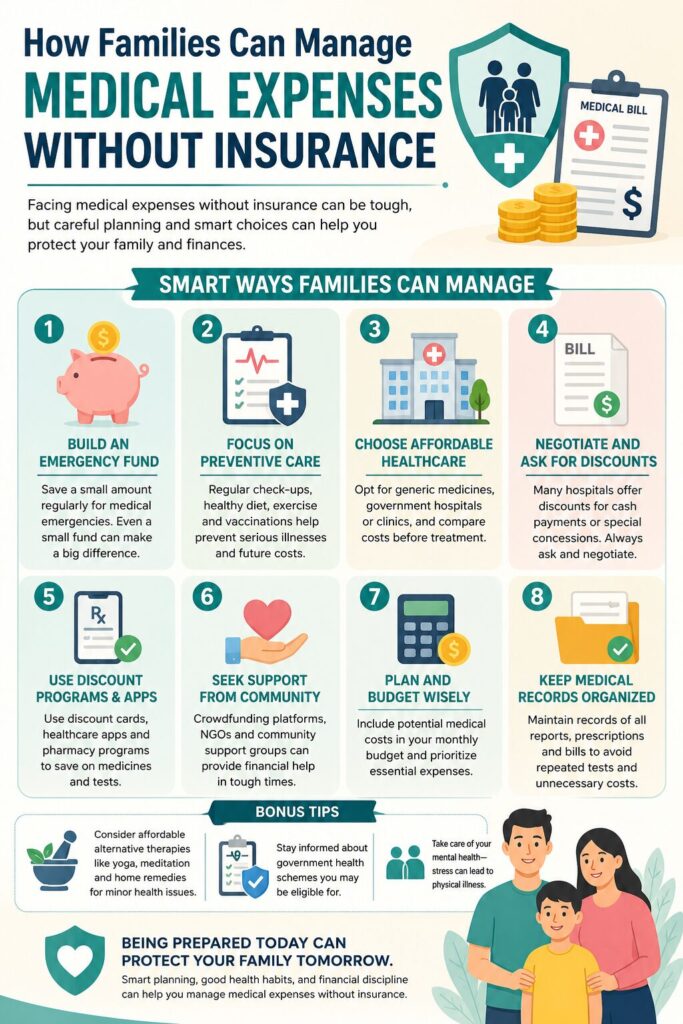

- Ways To Manage Medical Expenses Without Insurance

- 1. Start With Government Healthcare Schemes

- 2. Use Public Hospitals for Non-Emergency Care

- 3. Negotiate Bills and Audit Every Charge

- 4. Switch to Generic Medicines and Jan Aushadhi Stores

- 5. Build a Medical Emergency Fund

- 6. Pool Resources Through Family or Community Support

- 7. Explore Medical Loans and Credit Options With Care

- 8. Use Medical Crowdfunding for Large, Urgent Expenses

- 9. Seek Support From NGOs and Charitable Trusts

- 10. Get a Second Opinion Before Expensive Procedures

- Conclusion

- Frequently Asked Questions

Quick Summary

- Medical costs in India are rising faster than household savings and insurance coverage, making it difficult for families to manage medical expenses without Insurance.

- Families without adequate health insurance often struggle with hospital bills, medicines, surgeries, and rehabilitation costs.

- Government healthcare schemes, generic medicines, and negotiated hospital bills can significantly reduce expenses.

- Medical crowdfunding platforms like ImpactGuru help families raise funds online for urgent medical treatment.

- Financial planning, community support, and early action can prevent long-term debt during a medical emergency.

How Can Families Manage Expensive Treatment Costs Without Insurance

For millions of Indian families, a sudden hospitalisation, a cancer diagnosis, or a major surgery can wipe out years of savings overnight. What makes it worse is that about 30 percent of the population is uninsured.

If your family is facing high treatment costs without adequate insurance coverage, you are not alone, and you are not without options. This guide brings together the most practical, actionable strategies to help you manage expensive medical bills, protect your savings, and find the financial support you need.

Why Medical Bills Hit So Hard in India

Healthcare inflation in India is growing at roughly 12–15% annually, far outpacing general inflation. The cost of consultations, diagnostics, hospitalisation, and medicines has risen sharply over the last decade. Advanced treatments, ICU stays, cancer therapies, and organ transplants can run into lakhs or even crores of rupees.

At the same time, insurance premiums are climbing due to higher claim payouts. Many families still pay for treatment entirely out of pocket and resort to selling assets or borrowing at high interest just to keep a loved one alive. Without a plan, a medical emergency can become a financial catastrophe.

For families without sufficient health insurance, even a short hospital stay can create financial stress that lasts for years. This is why more people are now exploring alternative support systems like medical crowdfunding, financial aid programmes, and community-based fundraising.

Ways To Manage Medical Expenses Without Insurance

1. Start With Government Healthcare Schemes

Before spending a rupee out of pocket, check if your family qualifies for any government-backed health programme.

Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana is one of the most significant schemes available. It provides coverage of up to ₹5 lakh per family per year for secondary and tertiary care hospitalisation in both public and private empanelled hospitals. Eligible families can access major procedures at virtually no cost.

Other state-level schemes, such as Chief Minister’s health schemes, also offer significant coverage depending on where you live. Checking eligibility before approaching a private hospital can save your family enormous sums.

2. Use Public Hospitals for Non-Emergency Care

Public hospitals and government medical colleges provide treatment at minimal or no cost. While wait times may vary depending on the facility and type of care, public healthcare institutions can significantly reduce out-of-pocket expenses for planned procedures, follow-ups, and chronic disease management.

For many families, choosing a public hospital can be a practical and financially responsible way to manage medical expenses without compromising access to essential treatment.

3. Negotiate Bills and Audit Every Charge

Many patients and families may not realise that hospital bills can often be reviewed, clarified, and, in some cases, adjusted.

Request a detailed, itemised bill and review each charge carefully. Billing differences can sometimes occur due to duplicate entries, consumables, repeat tests, or administrative errors. If anything appears unclear, discuss it with the hospital’s billing department. Some hospitals may also offer payment plans or discounts for advance or lump-sum payments.

Asking questions and seeking clarity about treatment-related expenses can help families better understand and manage healthcare costs.

4. Switch to Generic Medicines and Jan Aushadhi Stores

The difference in price between branded and generic medicines can be enormous, sometimes as high as 80–90% for the same active ingredient. Generic medicines meet the same quality and efficacy standards and are widely available.

Ask your doctor specifically to prescribe generic alternatives. Pradhan Mantri Bhartiya Janaushadhi Pariyojana stores offer a wide range of medicines at significantly lower prices than retail pharmacies. For long-term treatments such as diabetes, hypertension, or cancer-support drugs, this switch can save lakhs over time.

5. Build a Medical Emergency Fund

Financial preparedness is one of the most underrated tools against medical debt. Ideally, every household should set aside three to six months of expenses in a liquid account, with a portion specifically earmarked for health emergencies.

For families that find this difficult to do all at once, a simple strategy is to invest ₹500–1,000 per month in a dedicated liquid mutual fund for healthcare. Over time, this creates a pre-paid health wallet that can cover minor to medium medical costs without touching your main savings or emergency reserve.

6. Pool Resources Through Family or Community Support

India’s family structure remains a natural safety net. In joint or extended families, each earning member contributing a fixed amount monthly, even ₹1,000, can build a meaningful shared health fund. When an emergency strikes any member, the pooled corpus is available immediately without the delay of loans or insurance claims.

Community organisations, religious trusts, and employer welfare funds are additional sources of support worth exploring before turning to debt.

7. Explore Medical Loans and Credit Options With Care

When savings and support systems fall short, structured borrowing is preferable to selling assets. Personal loans, loans against fixed deposits, insurance policies, or mutual fund units are all options that allow you to fund a medical emergency while keeping repayments manageable through EMIs.

Credit cards can also be useful for immediate payment at hospitals, providing 25–30 days of interest-free time, but they should be used with a clear plan for repayment to avoid high-interest debt.

Health-specific EMI cards offered by banks and NBFCs are another option that allows you to convert large hospital bills into manageable monthly instalments.

8. Use Medical Crowdfunding for Large, Urgent Expenses

For sudden, large treatment costs, particularly for conditions like cancer, organ failure, rare diseases, or major surgeries, medical crowdfunding has become one of the most powerful and accessible options available to Indian families.

ImpactGuru is one of India’s leading medical crowdfunding platforms, helping thousands of families raise funds for life-saving treatments every year. Through online crowdfunding, families can:

- Create a medical fundraising campaign in minutes with no upfront cost

- Share the fundraiser with friends, family, and the wider community across WhatsApp, social media, and email

- Receive funds directly and transparently with real-time tracking

- Access support from a dedicated campaign team that helps maximise reach

Medical fundraising through ImpactGuru has helped families cover costs for:

- Cancer treatment

- Kidney transplants

- Bone marrow transplants

- Heart surgeries

- ICU and emergency hospitalisation expenses

- Long-term rehabilitation and rare disease treatment

As a trusted crowdfunding India platform, ImpactGuru enables crowdfunding for medical treatment at a time when families need urgent financial support the most. Online crowdfunding has become especially important for patients with insufficient insurance coverage, expensive surgeries, or long-term treatment requirements.

If your family is facing a medical crisis and cannot bear the full cost alone, starting a fundraiser on ImpactGuru is free, fast, and has already changed thousands of lives.

9. Seek Support From NGOs and Charitable Trusts

Several NGOs and charitable organisations in India offer financial assistance or treatment support for specific illnesses. Tata Trusts, CanKids, and disease-specific foundations provide grants, subsidies, or connections to lower-cost treatment centres.

Research organisations relevant to your family member’s diagnosis. Hospitals affiliated with trusts sometimes have their own patient assistance funds that are not widely advertised; asking the hospital’s social worker or patient relations team is a good starting point.

10. Get a Second Opinion Before Expensive Procedures

Before agreeing to a costly surgery or an expensive treatment protocol, always seek a second opinion. This is not a sign of distrust, but rather responsible decision-making. A second opinion may reveal a more affordable treatment path, a less invasive procedure, or confirm that the original recommendation is indeed the best course.

Telemedicine platforms now make it easy to consult specialists across India at a fraction of the cost of in-person visits. For rural families or those in smaller cities, this is particularly valuable for accessing expert guidance without travel expenses.

Conclusion

A medical emergency should never become a financial emergency that your family cannot recover from. While health insurance remains the best first line of defence, it is not the only one, and for millions of families in India, it is not currently an option, making it essential yet difficult to manage medical expenses without insurance.

The strategies in this guide, from government schemes and generic medicines to negotiating bills, building a health fund, and using medical crowdfunding, give families real, practical tools to manage even the most expensive treatment costs.

Today, more Indian families are turning to online crowdfunding and medical fundraising platforms for urgent support during a healthcare crisis. Crowdfunding for medical treatment has become an important financial lifeline for patients facing expensive surgeries, cancer treatment, ICU stays, and organ transplants.

If you are currently facing a medical crisis and need immediate financial support, ImpactGuru can help you start a medical crowdfunding campaign quickly and securely. You do not have to face this alone.

Frequently Asked Questions

Families can manage medical expenses without insurance by combining government healthcare schemes, generic medicines, negotiated hospital bills, emergency savings, community support, medical loans, and medical crowdfunding platforms like ImpactGuru.

Medical crowdfunding is a way to raise money online for hospital bills, surgeries, medicines, cancer treatment, organ transplants, and other healthcare expenses through donations from friends, family, and the public.

Yes, trusted platforms like ImpactGuru provide transparent fundraising tools, secure payment systems, campaign tracking, and dedicated support teams for families raising funds for medical treatment.